Welcome to the February issue of Mutual Fund Observer.

We’re glad you’re here.

I’ve always been fascinated by the interplay of climate and culture, the way that our physical world seeps deep into our cultural bones. After years of The News from Lake Wobegon, Minnesota, gained an almost mythical spot in my vision of people in winter. For those of you who haven’t visited, the temps in Minneapolis hit -21 degrees Fahrenheit in January, and the force of the wind deducted another 30 degrees from that total. That’s low enough that your teeth ache and nose hairs freeze when you breathe in, about cold enough for them to declare their children can’t go out in shorts. There’s a sort of amiable stoicism about the challenge; Garrison Keillor’s story “The Stone” celebrates the habit of carrying a 25-pound rock with you when you go to visit friends on a winter’s night. You arrive out of breath and covered by a sheen of sweat and allow, “It was heavy, but it did its job… It kept me warm.” And the great upside of “a sub-zero winter? Well, at least it keeps the riff-raff out.”

These are the children of Scandinavia, inheritors of cultural lore that includes the Norse raiders we call Vikings and cultural traditions shaped by intense winters that made selfless cooperation into a survival value. Most Norse people were small farmers, but a minority of men periodically went viking; their raiding grew out of a farming-based society under resource pressure and was driven by profit, prestige, and need. Their reckless bravery was legendary. The Scandinavian heritage includes a deep commitment to community, captured in the Swedish concept of lagom (just right, balanced), Norwegian dugnad (communal work for the common good), and Danish hygge (coziness and community).

Both of those strands have been in evidence this year.

Image generated using ChatGPT

On numbingly cold days, day after day, Minnesotans stood up and stepped outside. They didn’t step outside to complain about the cold or petition the federal government for relief. They stepped outside because their neighbors — some born in Minneapolis, others in Mogadishu — needed someone to walk their children to the bus stop. Because immigrant families hiding from federal agents needed groceries. Because when masked officers with military weapons appear in your neighborhood, someone needs to be there with a camera and a whistle, documenting what happens next.

The children of the Norse, it turns out, inherited more than a tolerance for absurd cold. They inherited something about community, about collective welfare, about the quiet strength that doesn’t require bellicose chest-pounding or thuggish displays of power. The same cultural DNA that produced “Minnesota Nice,” that sometimes-mocked politeness and self-effacement, also produces a steel spine when circumstances demand it.

They’ve been noticed. Literally hundreds of folks in Davenport, not a hotbed of liberal activism, gathered on the streets with signs of solidarity. Protesters in Boston were recorded chanting, “We’re not cold, we’re not afraid, Minnesota taught us to be brave.” When the Minnesota National Guard was deployed in response to requests from the mayor and sheriff, those armed troops arrived bearing coffee and donuts and hand warmers for their brothers and sisters.

I’ve read my share of reveries on the passing of the Greatest Generation, most of them lamenting that Americans today are soft and self-absorbed, too whiny to summon the resolve their grandparents used to endure a Great Depression and still face down Hitler, then build a prosperous nation. I once suspected it myself. Now, I am not so sure.

Minnesota taught me better.

In this month’s Observer

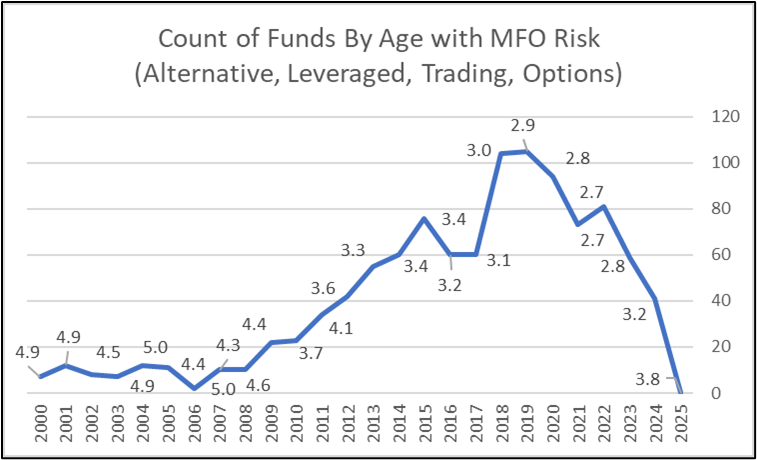

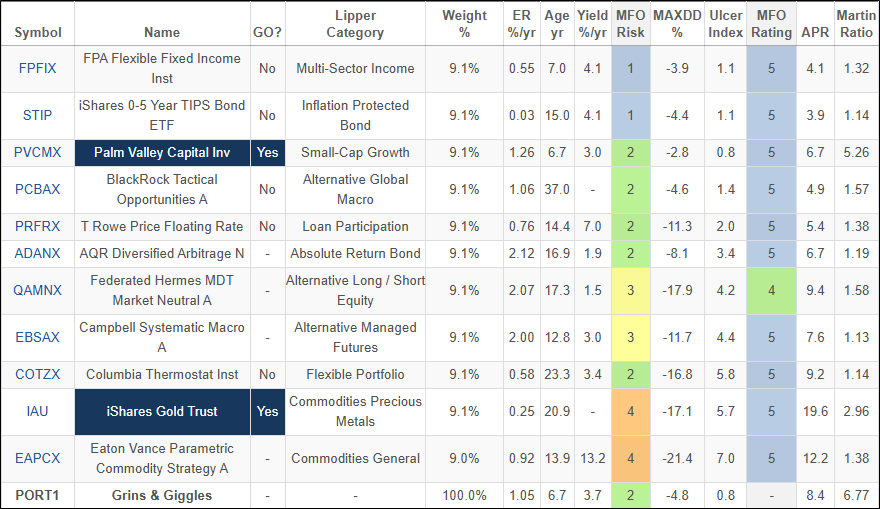

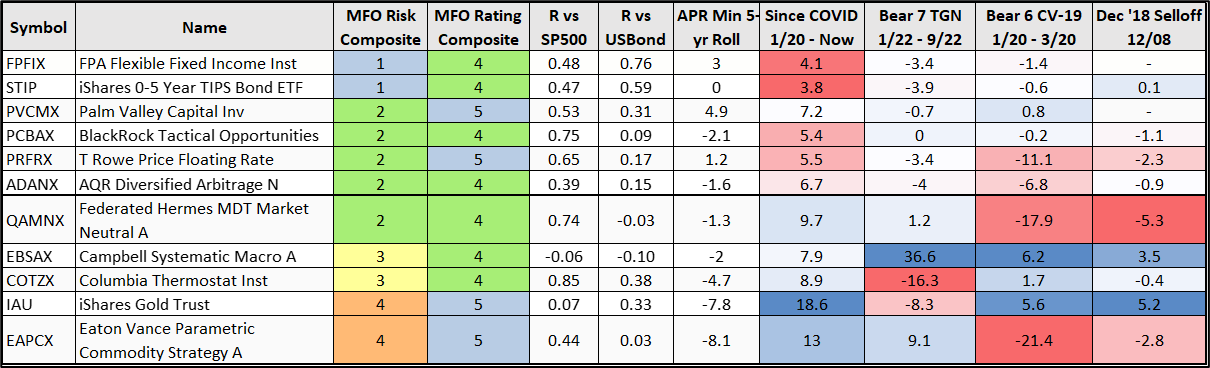

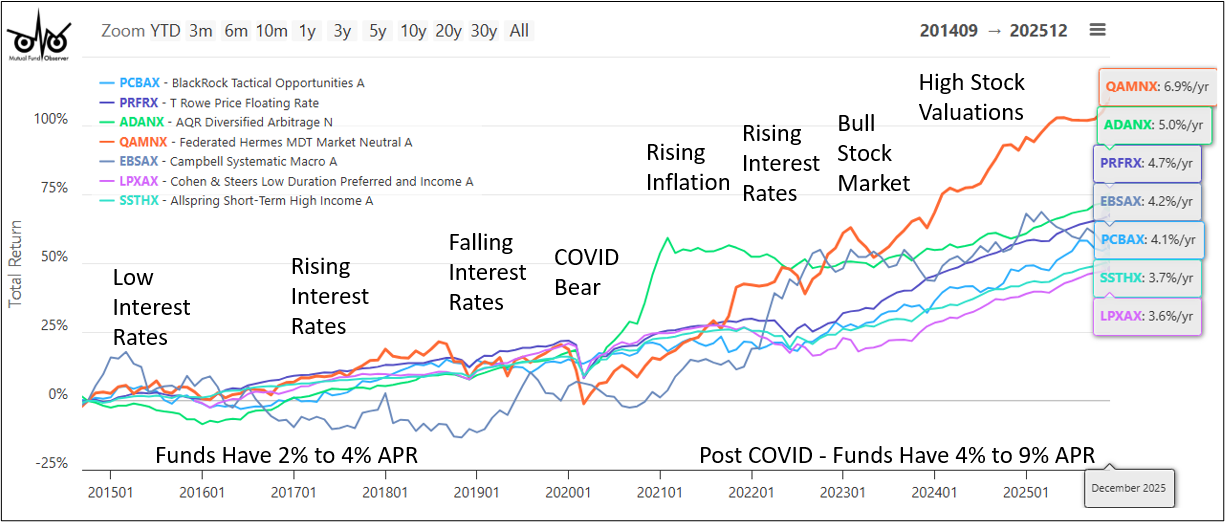

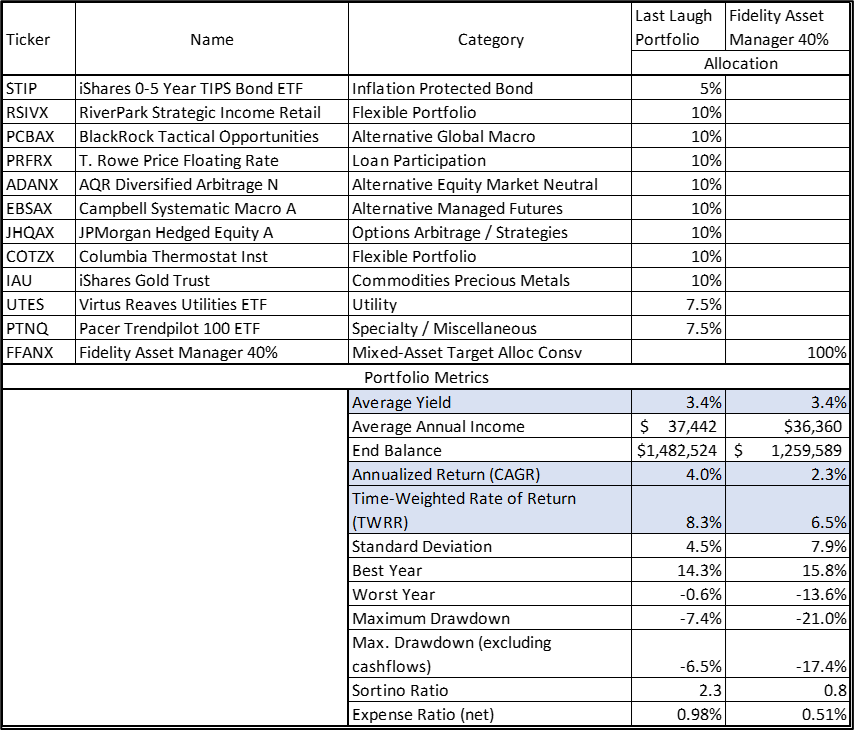

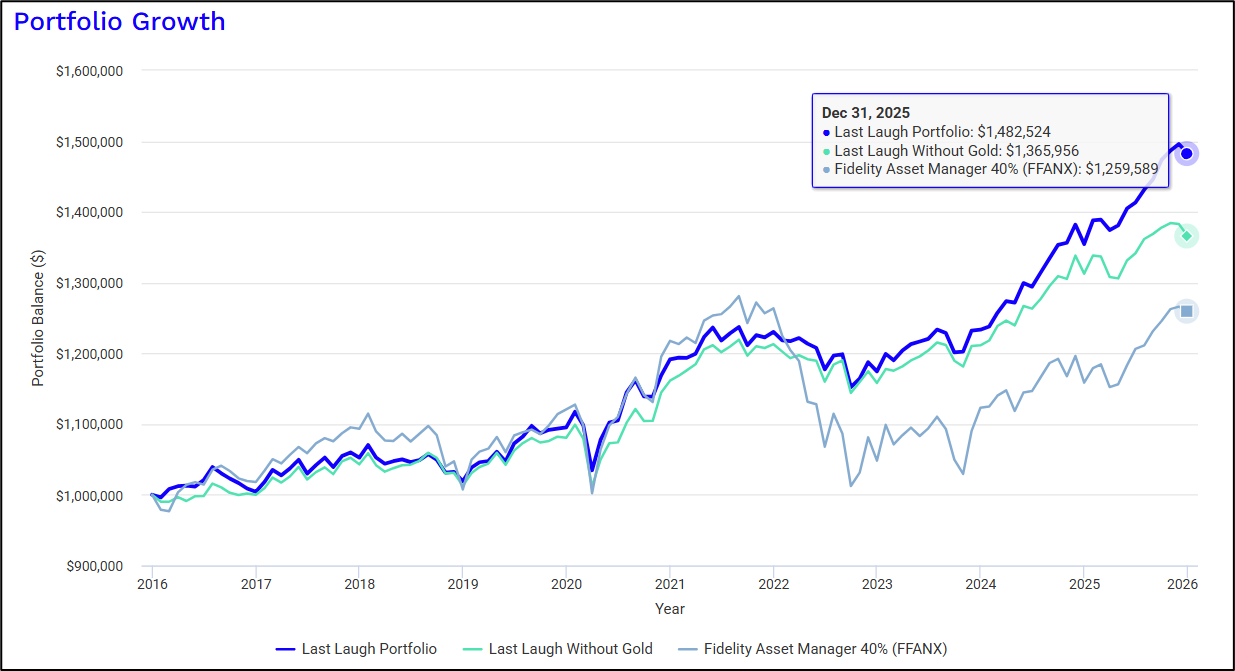

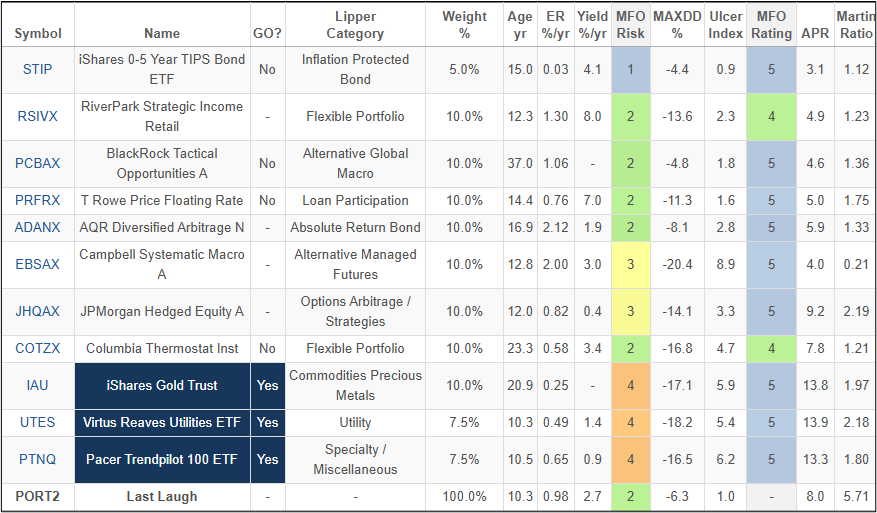

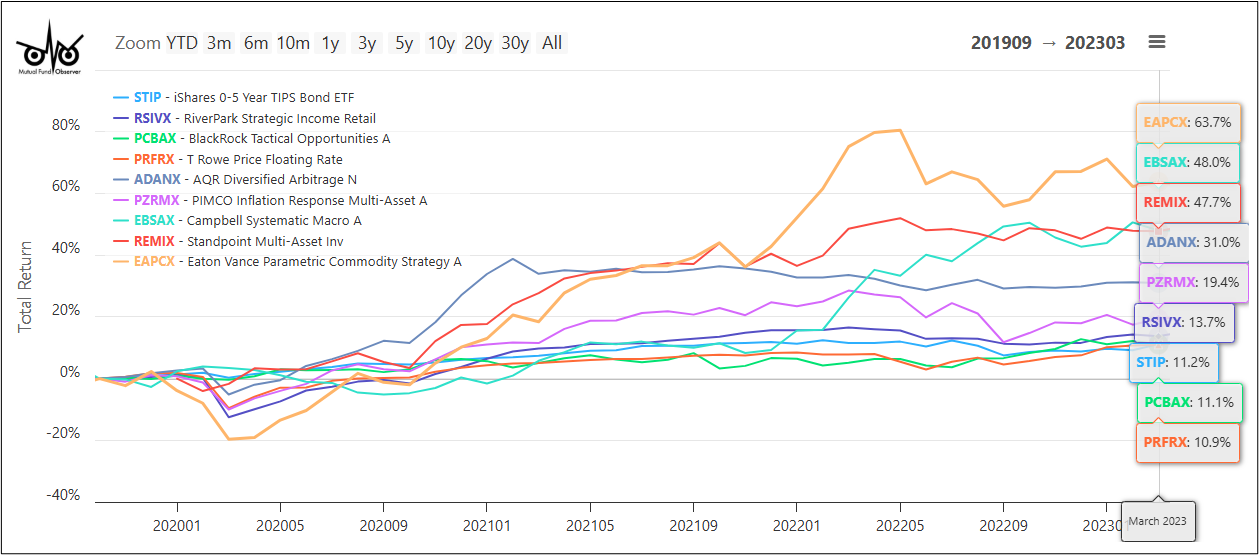

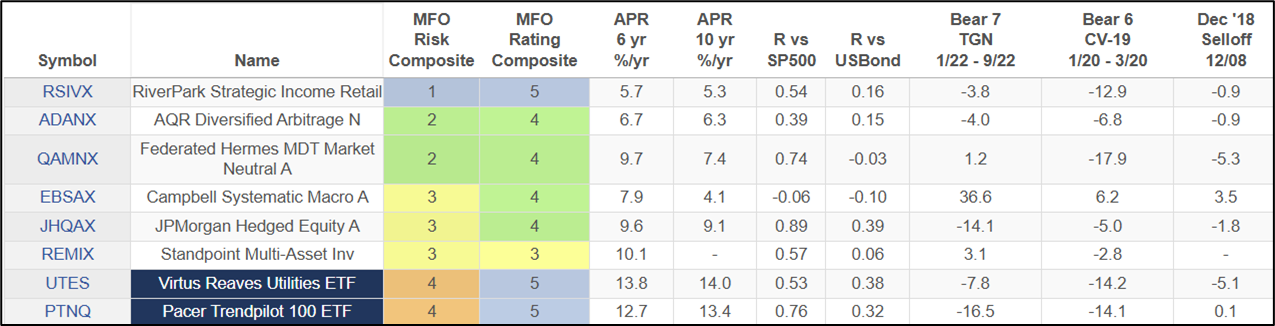

The One Uncorrelated Portfolio to Rule Them All by Slaying Inflation and Market Corrections, by our colleague Charles Lynn Bolin, tackles the challenge of building a portfolio that can weather both inflation and market corrections by searching through hundreds of alternative funds for options that zig when others zag. His “Grins and Giggles Portfolio” minimizes correlation between holdings over the past six years, while his “Last Laugh Portfolio” achieves 8.3% annualized returns with a maximum drawdown of just -6.3% over ten years. The secret? Four alternative funds that move independently of each other and traditional asset classes. Lynn’s analysis is grounded in consensus expectations for slow economic growth (2.2% GDP in 2026, falling to 1.8% by 2028) and elevated valuations that make diversification more critical than usual. He also sounds the alarm about financial innovations, from leveraged ETFs to options-based products, that pose risks even to investors who don’t own them, through the potential for financial contagion.

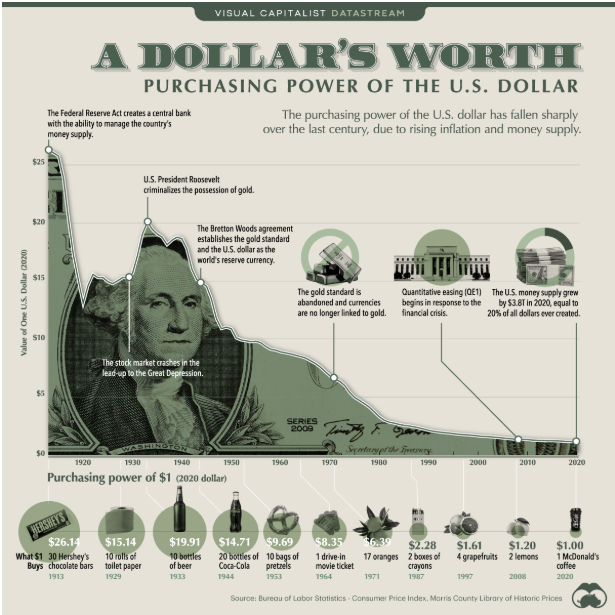

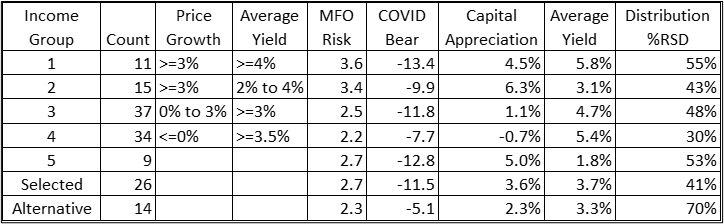

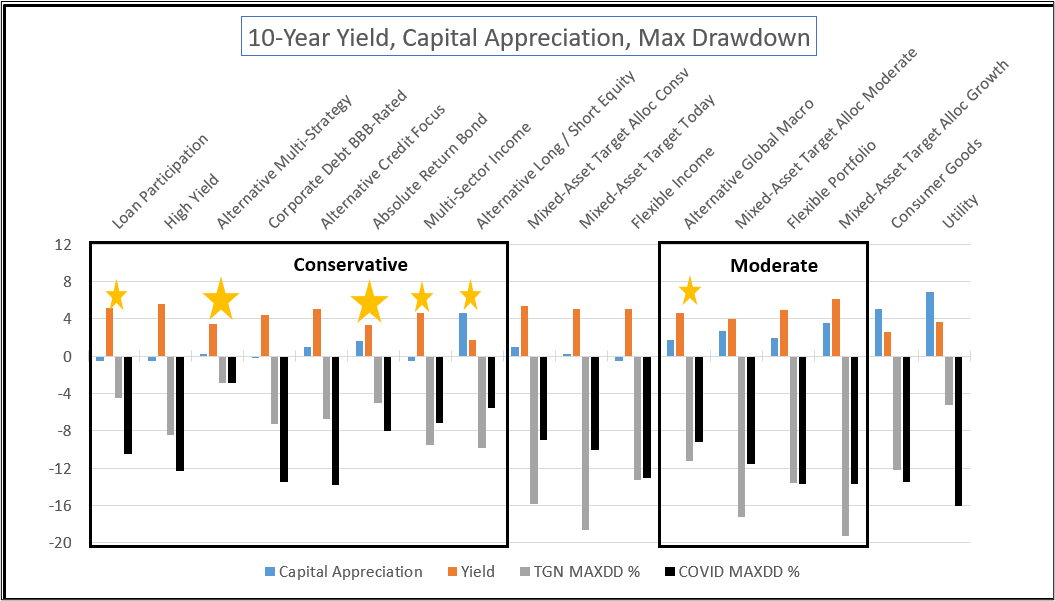

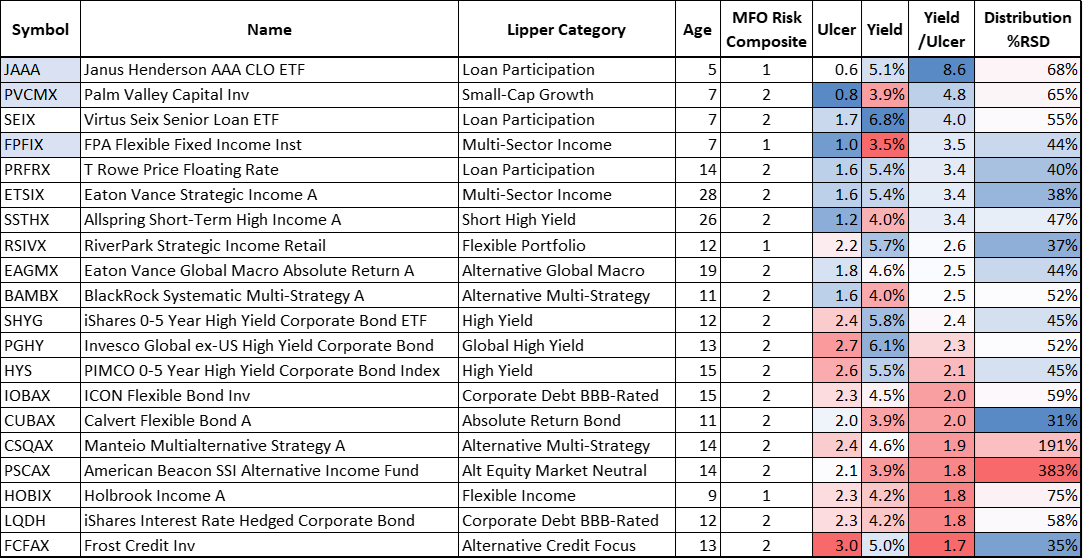

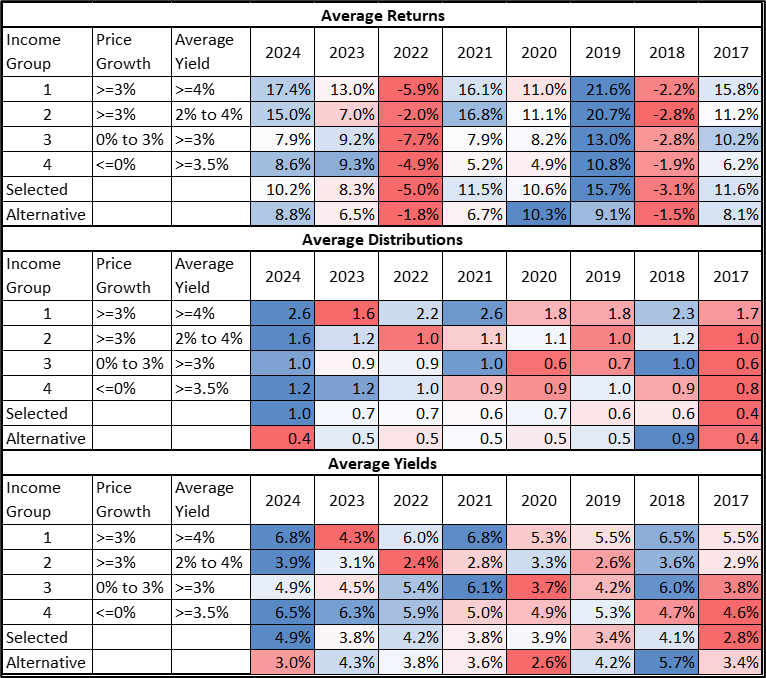

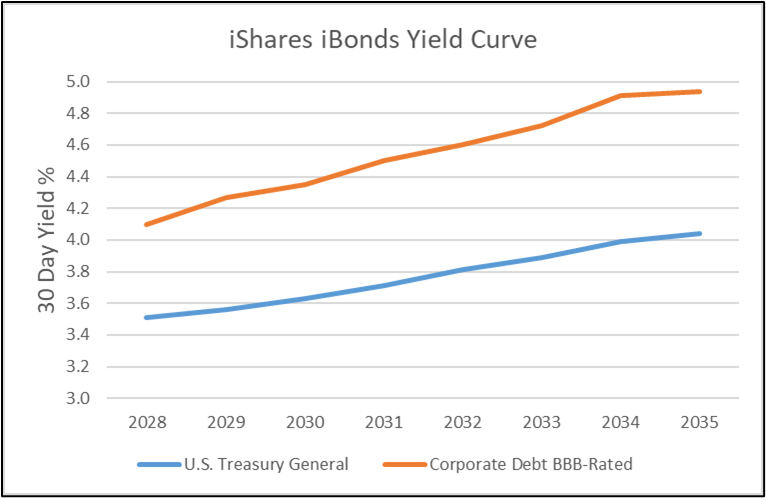

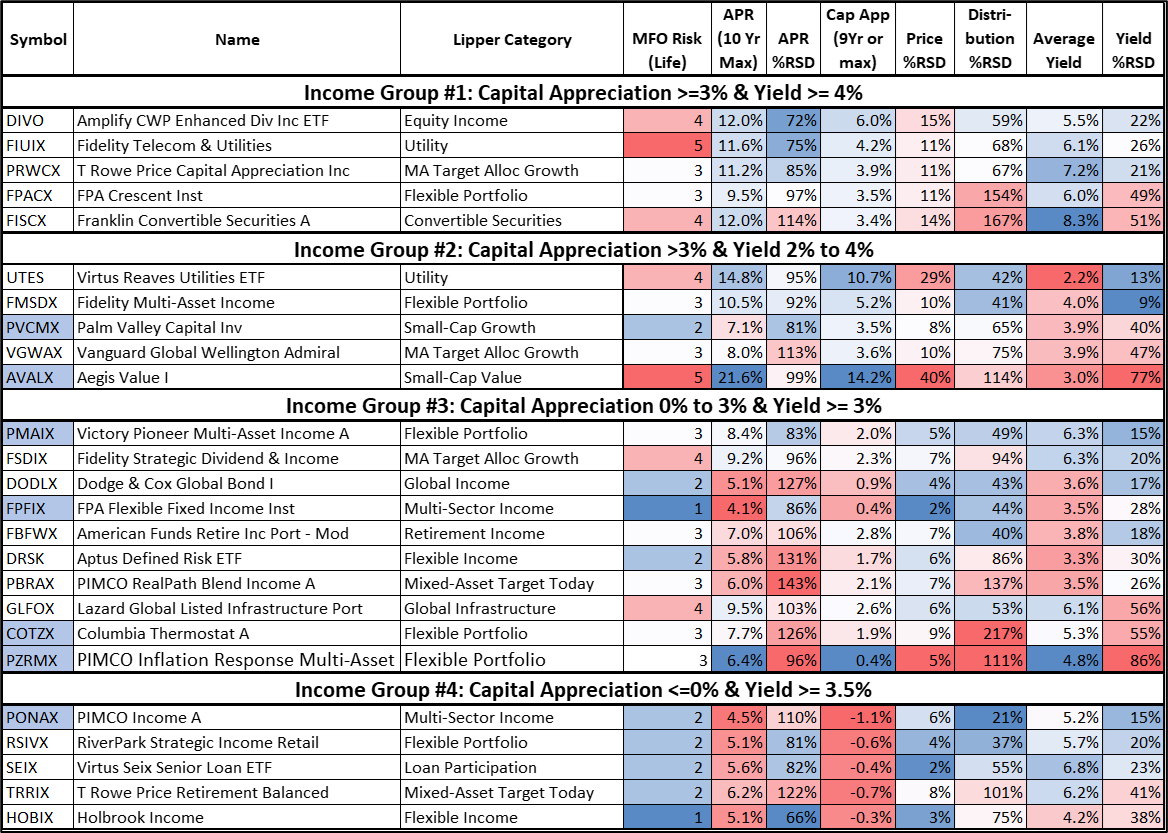

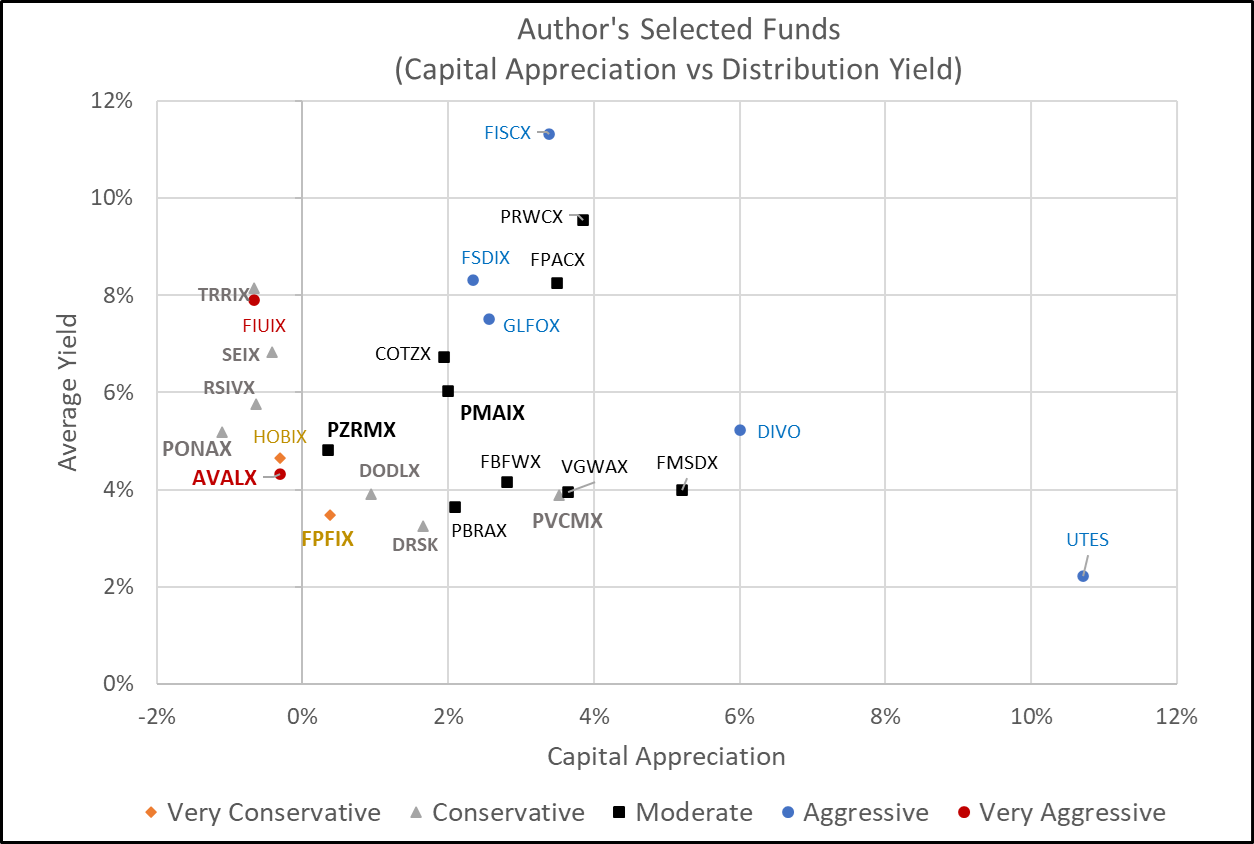

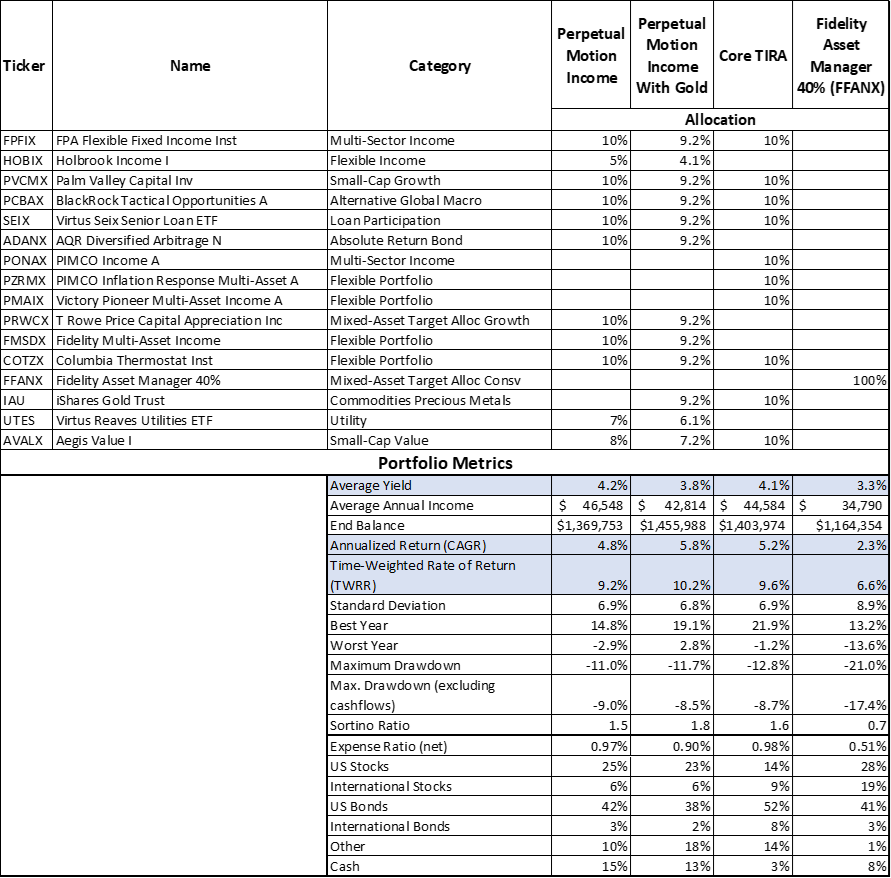

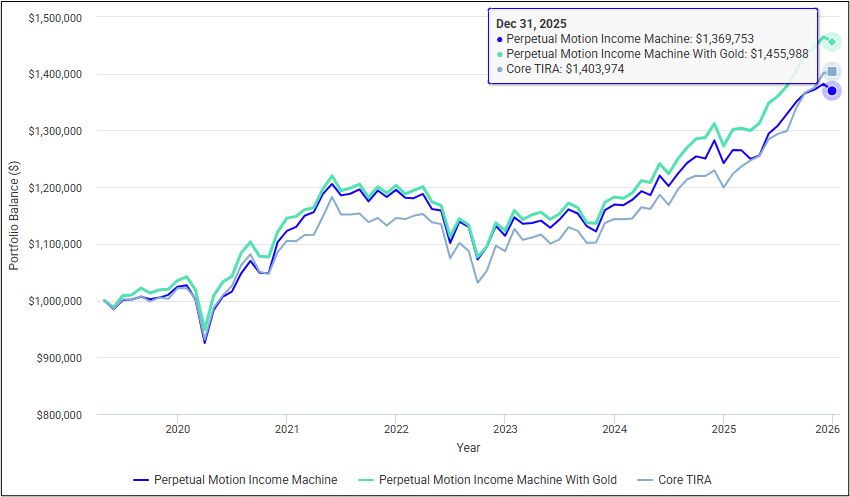

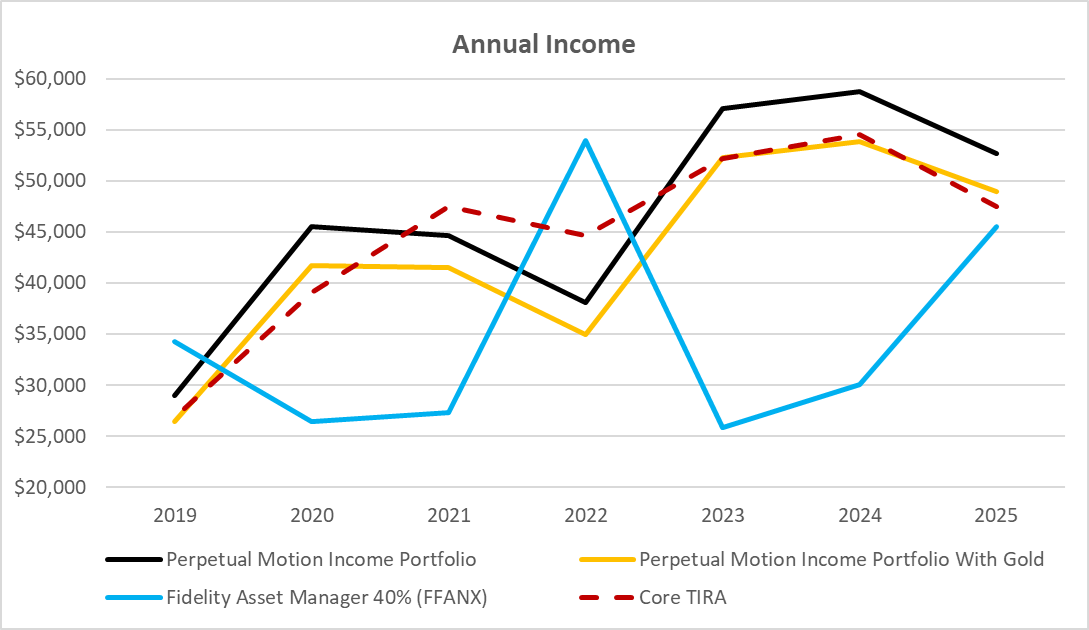

Perpetual Motion Income Machine, by Charles Lynn Bolin. Can you build an income portfolio that generates steady distributions while beating inflation? Lynn believes you can, targeting 7% minimum returns to cover 4% withdrawals plus 3% capital appreciation. He divides nearly 100 income funds into four groups based on capital appreciation and yield, identifying funds with high risk-adjusted yields and consistent distributions. The key insight: balance funds that fluctuate with interest rate cycles against those tied to stock market cycles to reduce sequence-of-return risk. Lynn’s research covers everything from loan participation funds to alternative credit vehicles, with particular attention to funds that maintained steady income through both the 2020 COVID crash and the 2022 rate-rising period. His approach emphasizes risk-adjusted yields rather than simply chasing the highest distributions, acknowledging that real inflation has averaged 2.3% since the 1980s and that three major secular bear markets over the past century have destroyed purchasing power for most portfolios.

Quality Worked in 2025, and failed spectacularly, looks at what “quality” investors did, and didn’t accomplish in 2025, and how to think about them in the years ahead.

A Letter to Layla is directed to the young trainer who is trying to coax Chip and me into being fit; we meet Layla at the YMCA gym twice a week, do our best to avoid embarrassing ourselves in public – I do a mean set of dead bugs – and try to stick with the program. Layla has been exceptionally thoughtful in structuring our efforts and, just recently, admitted that she would like to learn a bit about mutual fund investment so she can start moving in a healthy financial direction. This is my attempt to think about investing strategies for folks of Layla’s age – or my son Will’s – from the perspective of her work as a trainer.

The Indolent Portfolio, 2025, is the latest installation in my annual portfolio disclosure. It offers suggestions for how to build a low-maintenance portfolio and a three-fund alternative to my admittedly sprawling collections. (PS, the portfolio itself did just fine last year: stable, cash-rich, and up 14%.)

Our colleague The Shadow shares a wealth of industry news and foolishness, as ever, in Briefly Noted.

On the passing of Doug Ramsey

Doug and Diane

The folks at the Leuthold Group shared sorrowful news last week. I’ll let them speak for themselves:

It is with profound sadness that we share the news that our longtime friend, colleague, and partner, Doug Ramsey, passed away on January 22. This year, we celebrated Doug’s 20th anniversary with The Leuthold Group, though our relationship with him extended back to the 1990s, when he was first a research client. Doug’s encyclopedic memory and deep grasp of market history made him an ideal fit for our firm. In 2011, he became our Chief Investment Officer, leading our investment team and serving as a major contributor to our monthly research publication, Perception for the Professional. Doug will be deeply missed by all who had the good fortune to know and work with him.

Doug was an Iowa native, went to school in Cedar Rapids before heading to The Ohio State University to earn a master’s in economics. As a professional, he was equally famous for his extraordinary memory, his ability to make numbers speak, and the rarer ability to give the rest of us some clue about what they said. He and his beloved Diane met in Iowa City, were married in 1994, raised children and golden retrievers with equal aplomb, did Minnesota stuff – some substantial fraction involving rods, reels, rivers, lakes, and forays in the dead of winter to the only open water available (just downstream of the nuke) by way of recreation. Doug had been suffering some unrelated (?) pains in recent months, and the other Leuthold folks stepped in to make sure that there was no stumble. He was felled by a brain aneurysm at age 59.

It’s easy to think of investment advisers, even boutiques like Leuthold, as faceless automata. It’s an illusion that crumbles when you’ve had the chance to chat for hours over the phone or to sit with folks in their breakroom, sipping coffee (if you visit Minnesota, you’re actually legally required to develop a taste for black coffee and quiet conversation) and nibbling pastry. There you discover that Doug was funny and understated, reflective about his industry, his beloved city, his clients (aka “you”), and the colleagues with whom he’d shared decades. Paula Mikl, one of those colleagues, lost her dad last fall, which she could sort of manage. But “Doug’s passing seemed to cut even deeper; there were no signs, just sudden finality. We are a small, close-knit group; we are hurting at the loss of our friend and partner, but finding a way to move forward.”

Infrastructure: The Trillion-Dollar Distraction You’re Ignoring

While ChatGPT was writing your emails, geologists confirmed Manhattan is sinking under the weight of its own skyscrapers, requiring billions in flood barriers and foundation reinforcements. Miami is sinking faster and faces the bill first. 43,000 American bridges continued their slow collapse. (They’ve been recognized as “the most dilapidated on Earth” so … uhh, we’re number one!). Our western snow drought just hit record levels, threatening water supplies, and the electric grid needs $2 trillion in upgrades before your AI dreams can plug in. Uncomfortable reminder: the physical world still exists, requires continuous investment, and won’t maintain itself while we chase the next magnificent stock. Infrastructure funds gained 20.5% in 2025, crushing tech-heavy benchmarks, but who noticed?

BNY Mellon Global Infrastructure Income ETF led the category, up 37.8%, beating peers by 17.4 points. Their media team promised insights has sort of ghosted us … so we’ll profile them anyway in March alongside Brookfield Next Generation Infrastructure, iShares Emerging Markets Infrastructure, and Lazard Global Listed Infrastructure (a Great Owl fund). Consider this your heads-up: trillions must flow into roads, bridges, water systems, and power grids in the years ahead, regardless of what happens with artificial intelligence. Trillions must flow into roads, bridges, water systems, and power grids in the years ahead, regardless of what happens with artificial intelligence.

Thanks, as ever …

To The Faithful Few whose monthly support keeps the lights on and supports up: Gregory, William, William, Stephen, Brian, David, Doug, Altaf, Wilson and the good folks at S & F Investment Advisors.

And to a host of others who’ve offered support in the past couple of months. Because Chip and I were on the road over New Year’s, we weren’t able to properly recognize the generosity of Rae from Cincinnati, Mark from Swartz Creek, Marc from Maryland, Charles from Indianapolis, Binod from Houston, the Ellie and Dan fund, Kevin from Brooklyn, Joseph from Centennial, Sunny from Westlake Village … and an anonymous bear-shaped bull! And, in January, we add many thanks to Wayne, our first donation through the PayPal Giving Fund, Kathleen from Redwood, Gary from Sacramento, and Sharon from Washington. We appreciate your support!

We reminded readers this month that your investment advisor doesn’t need you nearly as much as the world does. If you’re disposed to act upon that suggestion, consider contributing to a needy teacher (K-12) through Donors Choose. You choose the project and the amount, whether its $5 or $500. This month, I chose to help provide the final bit of support needed to complete a project in St. Paul, Minnesota, Minneapolis’s twin sister.

When I did, Donors Choose reminded me that they are making a special request to support the teachers and kids in the Twin Cities:

The Minnesota Students & Teachers Fund will provide urgent resources to Twin Cities-area educators tirelessly working to provide stability and safety in their community. Make your donation to the Minnesota Students & Teachers Fund, and we’ll direct your gift to meet the most pressing teacher needs in the Twin Cities. These resources will be distributed quickly to support classrooms where support is needed most.

And so, I did. You might consider it if you’re not predisposed to trudge out in weather that even Minnesotans allow, “is a might nippy.”